SPONSORED BY COLLEGE AVE

You've done the FAFSA. You've reviewed the financial aid award letters. After scholarships, grants, and federal student loans, there's still a gap to fill. Now what?

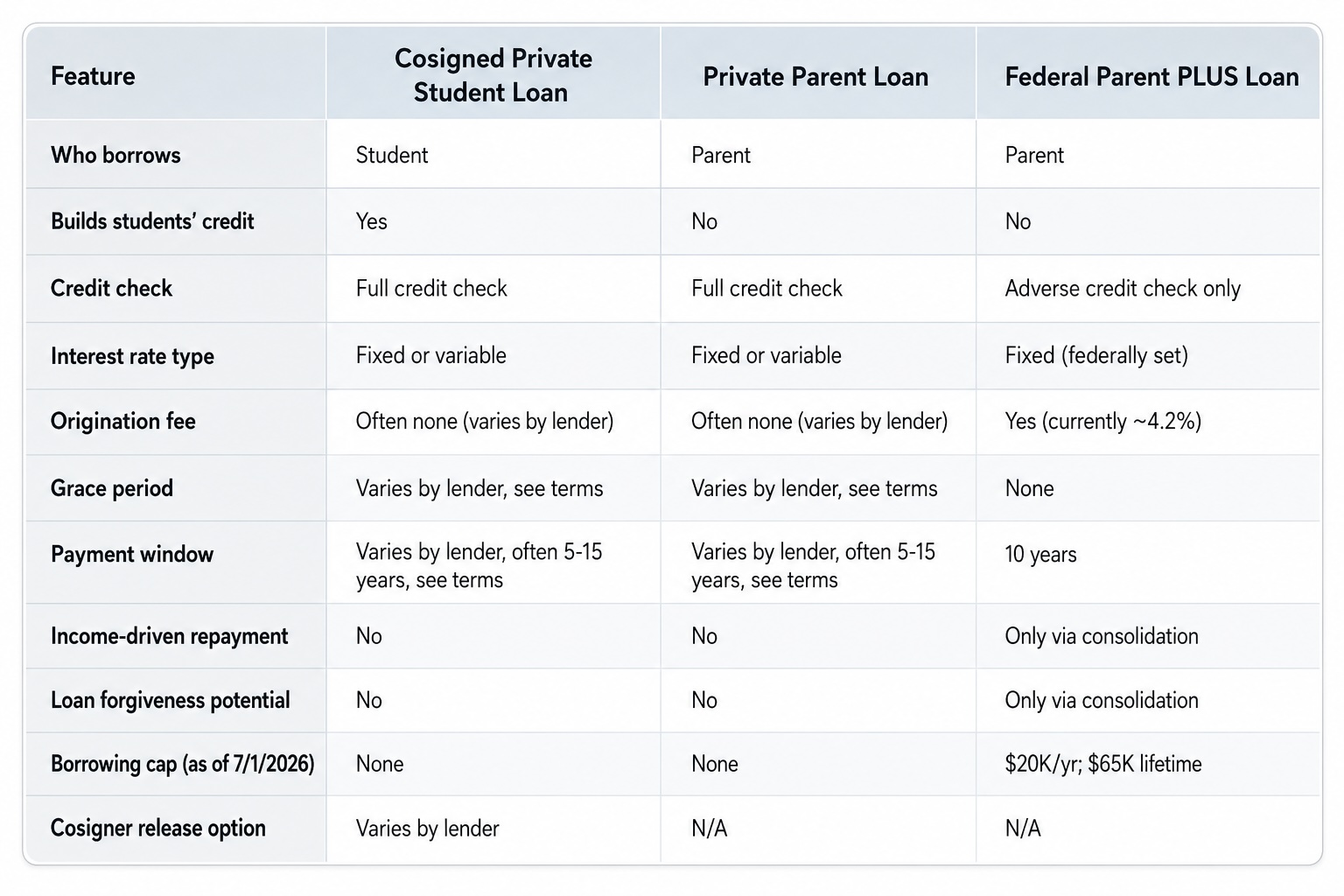

For many families, the next step has been either a federal Parent PLUS Loan or a private loan (either for the parent or cosigning in the student’s name). But this isn't always a straightforward choice, especially in 2026, with new federal rules coming into effect that will change how much parents can borrow under the PLUS program. Before exploring private options, it’s worth understanding what’s changing with Parent PLUS loans and why.

A Parent PLUS loan is a federal loan available to biological or adoptive parents of dependent undergraduate students. Unlike other federal student loans, which go to the student, a Parent PLUS loan is in the parent's name, and the parent is solely responsible for repayment. Grandparents and legal guardians do not qualify unless they have legally adopted the student.

What's changing in 2026: As of July 1, 2026, Parent PLUS loans are capped at $20,000 per year per student, with a lifetime limit of $65,000 per student. These are maximum caps; a PLUS loan cannot exceed the student's cost of attendance minus other financial aid. Parents will also not be able to borrow until the student has first maxed out their federal Direct Loan limit. Previously, parents could borrow up to the full cost of attendance minus other aid received. Married or divorced, each eligible parent may apply separately for a Parent PLUS loan for the same student. Because these loans are capped per student, if more than one eligible parent is applying for a Parent PLUS loan for the same student, they will not be allowed to exceed these totals.

Get the latest Parent PLUS rates and terms at studentaid.gov.

Pros of Parent PLUS Loans

Cons of Parent PLUS Loans

For a deeper look at how parent loans work and what to consider before applying, see College Ave's guide: What Is a Parent Loan?

Once federal loan options are maximized, private loans can help fill what's left. There are two main paths, and the right one for your family depends on who takes on the legal obligation — the student, the parent, or both.

Most college students have a limited credit history, and many private lenders may require a cosigner to qualify or to secure a competitive rate. When a parent cosigns, both the student and parent take equal responsibility for the loan. It appears on both of their credit reports.

This matters in both directions because both parties share equal legal responsibility for repayment. On-time payments help to build the student's credit history from day one. Missed payments affect both the student's and the cosigner's credit scores.

The practical upside of cosigning, compared to a parent loan, is that a portion of the obligation lives in the student's name, giving them a direct stake in repayment. Some loans also offer a cosigner release, so that once a student has shown themselves to be financially responsible by demonstrating a consistent payment history, and meets other lender-specific requirements, the parent can remove themselves from the loan.

For a detailed side-by-side look at cosigning vs. taking out a parent loan, see College Ave's guide: Cosigning a Loan vs. Taking Out a Parent Loan.

Pros of Cosigning a Private Student Loan

Cons of Cosigning a Private Student Loan

Explore Private Student Loans from College Ave

If a parent prefers to directly take on the borrowing responsibility without involving the student’s credit, a private parent loan may be the right fit. Like a Parent PLUS loan, a private parent loan is taken out entirely in the parent’s name. The student has no legal repayment obligation, and the loan does not appear on their credit report.

Private parent loans are offered by banks, credit unions, and private student loan lenders, and can be used to cover tuition, housing, books, and other school-related costs.

Private parent loans are credit-based. Interest rates, which can be fixed or variable, are determined by the lender based on credit history and income review. Borrowers with strong credit may find that private parent loans offer more competitive rates than the federal Parent PLUS loan, particularly once the Parent PLUS loan origination fee is factored in. According to College Ave, their parent loan rates currently range from 2.59%–17.99% APR, which includes an autopay discount. Get the latest rates here. † To gauge whether a private student loan rate is competitive, apply with multiple competitors and compare each offered APR, which includes interest and fees. You should also take into account any rate discounts offered and repayment terms when comparing competitors.

Pros of Private Parent Loans

Cons of Private Parent Loans

Explore Private Student Loans from College Ave

Your best choice depends on your credit profile, financial goals, retirement timeline, and how students and parents plan to share repayment responsibility. These questions can help frame the conversation:

Start with federal loans in the student’s name first — they offer fixed rates, borrower protections, and access to repayment programs that private loans don't. Once those are maximized, private loans or Parent PLUS loans can help close what's left. Whether a parent cosigns a private student loan or takes out a parent loan option, going in with a clear understanding of who is responsible, what the true cost is, and how it fits into the family's broader financial picture makes all the difference. With new federal borrowing changes taking effect in 2026, it's worth comparing all your options well before the school year begins.

Explore Private Student Loans from College Ave

Key Takeaways

Sponsored by College Ave. If you're interested in becoming a partner of The Princeton Review and sponsoring educational content, click here for details.

† College Ave rate ranges (2.59%–17.99% APR) reflect rates current at time of drafting and include an autopay discount. Rates are subject to change.

†† College Ave does not charge origination fees.

Connect with our featured colleges to find schools that both match your interests and are looking for students like you.

Join athletes who were discovered, recruited & often received scholarships after connecting with NCSA's 42,000 strong network of coaches.

170,000 students rate everything from their professors to their campus social scene.

Opt-Out Signal Honored

Opt-Out Signal Honored